In the realm of personal finance, emergency funds are all the rage. Comparing emergency fund account sizes is practically a measuring contest among influencers.

The point of this article is NOT to debunk the need for emergency savings. I’m a big fan of saving money outside of a 401k or retirement program.

Theoretically, it seems like a pragmatic idea to have a sizeable cushion of cash to solve life’s most expensive surprises. But have you ever calculated the opportunity cost of keeping so much money in a low margin bank account? Let’s take a closer look.

Emergency Fund Definition

First of all, what exactly is an emergency fund?

If you’re a newcomer to the personal finance space, you may appreciate a formal definition of an emergency fund. So here it is:

An emergency fund is money set aside for unexpected events.

Yes, its that simple.

You need an emergency fund because you don’t know what will happen in the future, like a job loss, HVAC failure, or a deadly pandemic.

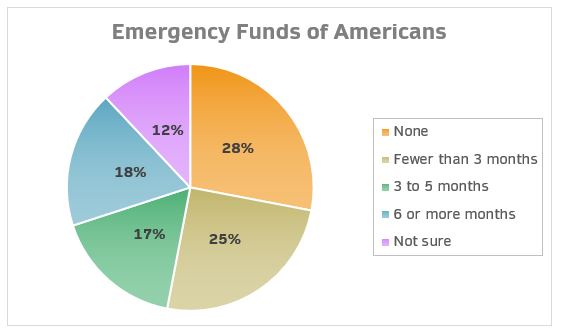

Per Bankrate[1] data, 28% of Americans had zero money saved for emergencies, as of July 2019. That was before the 2020 Covid-19 pandemic hit. Ouch.

Where to Keep Emergency Funds

Because emergency funds should be cash one can easily access, experts recommend you keep the funds in a bank account. You want to be able to access the funds if necessary, but you don’t want them to be too easy to access. Also, you’ll want to earn some interest on those funds, even if its not much.

A high-margin money market account is recommended (more on this later).

Because let’s face it, if you keep the funds in your checking account you’re going to spend them. Am I right? So wherever you choose to deposit them, don’t do that.

When to Use Emergency Funds

Emergency funds should be used for urgent and necessary situations only. Not for retail therapy, splurges, down payments on cars you shouldn’t be buying in the first place, or on other frivolous impulses.

Emergency Fund Size

Most personal finance influencers will tell you to keep six months of living expenses in your emergency fund. As a baby step to improve your financial situation, I get how this type of advice makes sense for some people.

If you’re following the Dave Ramsey recommendation, building your emergency fund is Baby Step #3, after saving $1,000 and paying off your debt. On some level, Baby Step #3 is an introduction into the idea of saving money outside of a retirement account, and a way to prevent you from needing to use a credit card in an emergency situation. Bravo!

Probability of an Emergency

If your financial situation is stable and you earn more money per month than you spend, you probably don’t need to use an emergency fund frequently. Ask yourself the following questions:

- How often will you need more cash than a month’s worth of living expenses immediately?

- How often will the need for immediate cash coincide with a significant drop in the stock market?

- Would it be feasible for you to wait 2 days to access more than 1 month’s worth of cash for an emergency?

If you don’t think you’ll need more than one month of cash at a time, even in an emergency, you could deposit some of your emergency fund money into a brokerage account.

Each person has a different risk profile and will need to consider their comfort level with having some cash in liquid form, and the rest of it in slightly less liquid form (stocks).

Let’s move on to the fun stuff.

Scenario Testing

If your financial situation is truly stable, you likely won’t need more immediate cash than one month of living expenses ever. But let’s assume something does pop up, and that it happens once in 5 years, or once in 10 years. We will further assume that this emergency of yours is associated with a stock market plunge of 20%.

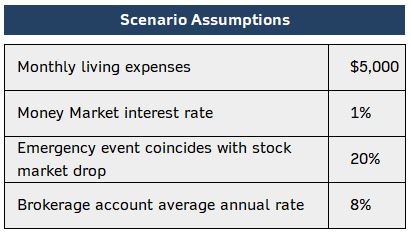

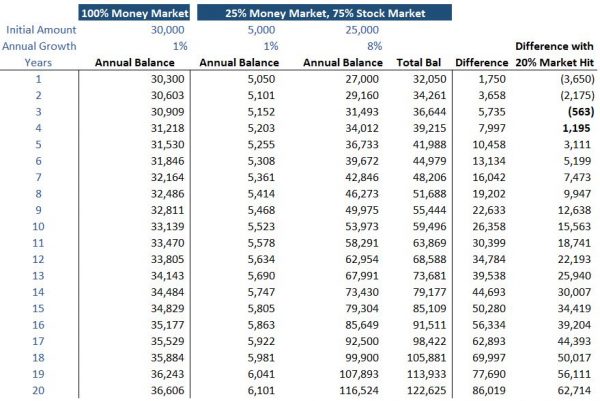

In our scenario, your living expenses are $5,000 per month.

With an emergency fund of six months, you would have a balance of $30,000 in your bank account. In a high yield savings account paying an average of 1% interest, you would have $31,530 after 5 years, and $33,139 after 10 years. This assumption becomes our baseline.

Let’s assume that instead, you chose to keep only 1 month of living expenses in your emergency fund, and deposited the rest into a brokerage account yielding an average of 8% per year.

So $5,000 at 1% and $25,000 at 8%.

In Five Years

In 5 years, you would have $5,255 in your savings account and $36,733 in your brokerage account for a total of $41,988.

Let’s assume at this point, the unexpected happens. A global pandemic hits, the stock market drops 20%, and you lose your job. You need to liquidate your positions and withdraw your cash to pay bills in month 2, after your emergency funds are spent.

Since the market dropped 20%, you now only have $29,386 in your brokerage account, and prior to paying any bills, you have $5,255 in your bank account, for a total of $34,641.

Even though the market dropped 20%, you still made $3,111 more than if you had kept the full $30k in a bank account. And although its never fun selling positions at a low, you still grew your total balance much more by investing 75% of your total savings.

In Ten Years

Let’s run the same scenario over 10 years.

If you kept all of the funds in your savings account, you would have $33,139 in 10 years using an average interest rate of 1% per year.

If you kept $5k in your savings account and $25k in your brokerage account, in 10 years you would have $5,523 in your savings account and $53,973 in your brokerage account for a total of $59,496.

Let’s assume at this point the unexpected happens. A global pandemic hits, the stock market drops 20%, and you lose your job. You need to liquidate your positions and withdraw your cash to pay bills in month 2, after your emergency funds are spent.

Your brokerage account balance dropped 20% to $43,179. If you combine that with your bank balance of $5,523, you now have $48,702 in total savings to use. Even with the market drop, your yield is $15.6k more than if you kept your funds in a bank account, a difference of 50%.

Simmer on that for a moment. 50%

Breakeven Timeframe

So where do we break even?

If an adverse event causes a stock market drop of 20%, you would lose money in years 1-3 by investing 75% of your emergency savings in the stock market, and then needing to liquidate it to spend. This assumes you would liquidate all of it.

The breakeven timeframe happens somewhere between years 3 and 4, with years 4 and on becoming profitable, even with a market drop of 20% coinciding with the need to withdraw your funds.

Opportunity Cost

If you have a stable job and aren’t worried about a loss in income in the next few years, ask yourself if the opportunity cost of keeping six months of cash in savings is really worth it. However, if you are a retiree, soon to retire, or have a job that doesn’t provide regular paychecks, keeping a sizeable cash balance may make sense.

Keep in mind, brokerages like TD Ameritrade have accounts that provide a debit card, should you ever need to spend your funds quickly. The only delay would be in closing a stock position and waiting for the funds to settle. When you buy or sell stocks, it takes two days for cash from those trades to become available.

Two days to access 5 of your 6 months of savings. That’s it.

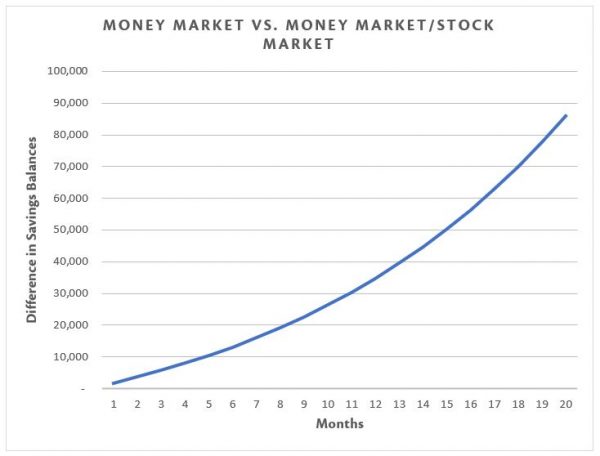

Look at the chart below to see how much it would cost you to leave $25,000 of your emergency fund in a money market account. Then ask yourself – is it worth it to keep it in the bank?

An Alternate View

Its paramount to have a sizeable savings built up outside of retirement accounts, for many reasons beyond (and including) emergencies.

I keep one month of emergency funds in a high-margin money market account (it currently yields less than 1% per year). I keep the rest of my post-tax savings in various places, including stocks, options, and in less liquid accounts like Lending Club and Diversyfund.

Paying yourself money outside of your retirement account gives you flexibility to retire early, take a mini retirement, buy real estate, or make a career change. Locking up all of your savings in a 401k account that you can’t access until age 65+ hinders your ability to control your life and lifestyle.

Investing your money in a manner that yields a decent return is one of the primary money lessons from The Richest Man in Babylon. Lesson #3, “Make thy gold multiply”, is best followed by using a mix of money market and stock market investments for emergency funds.

Ultimately, YOU decide the allocation that makes the most sense for your income stream and lifestyle. Your decision should be made with a full understanding of the potential cost of your choice.

How large is your emergency fund and where do you keep it?

[1] https://www.bankrate.com/banking/savings/financial-security-june-2019/#:~:text=Nearly%20three%20in%2010%20(28,months’%20worth%20of%20living%20expenses.